Portfolio Manager

• Insight

The neobank era has arrived

Neobanks, which are challenging traditional banks with their digital-only banking services, have been growing fast and grabbing market share from conventional rivals worldwide. Now profitability is the focus and we believe the neobank era has truly arrived.

Authors

Portfolio Manager

Portfolio Manager

FinTech/New World Financials Analyst

Summary

- Common elements but unique business models

- Diversified revenue streams underpin positive outlook

- Focus shifts to profitable growth as opposed to profit at any cost

Neobanks saw rapid customer growth with the pandemic’s shift to digital banking. However, higher interest rates since 2022 have affected availability of funding for fintech in general and raised concerns over business models of neobanks and their ability to monetize a growing customer base. According to BCG, only 23 out of 453 global digital challenger banks in 2023 were operationally profitable.

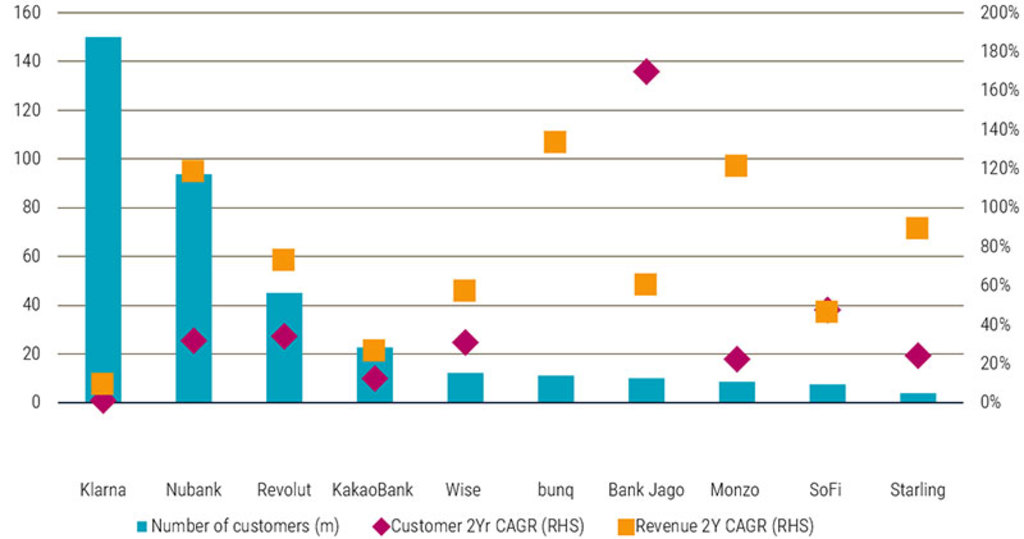

Figure 1: Neobanks are growing revenue fast

Source: Robeco, company data, end December 2023

The challenging backdrop has prompted neobanks to shift from ‘growth at all cost’ to profitable growth and sustainable operations. Customer acquisition has decelerated somewhat from pandemic highs, but revenues continue to rise impressively. According to BCG, challenger banks were star performers posting revenue CAGR of 78% in 2021-2023 compared to 14% average for global fintech, and 21% excluding crypto- and China-exposed fintechs.

In 2023 a number of leading neobanks demonstrated record profitability

In 2023 a number of leading neobanks (Revolut and Starling) demonstrated record profitability and several players reported full year of profits for the first time (Monzo and bunq). The positive trend continued into 2024 with Dave, MoneyLion, Chime and SoFi turning to profitability in recent quarters in the US.

Figure 2: Profitability improving (in USD millions)

Source: Robeco, company data, end December 2023

Regional focus

Neobanks have taken unique paths to scale and profitability depending on the starting point including geography, market characteristics, customer focus and product strategy. The operating and regulatory environment differs across countries. In the US neobanks tend to be niche, focus on payments and operate in partnerships with banks. Chime, for example, is partnering with two US banks and its revenue stems primarily from interchange fees.

In the EU neobanks face tough competition with a high number of neobanks per capita, low interchange fees (capped at 0.2% for debit and 0.3% for credit) and increased regulatory scrutiny. In Brazil, on the other hand, the central bank and regulators created infrastructure (instant payment system Pix) enabling fintech solutions to scale with a number of success stories including Nubank (a neobank), Creditas (a lending platform), Dock (a fintech infrastructure provider), and Ebanx (a payments provider).

Markets with a significant underbanked population offer attractive growth prospects. Nubank is a good example of a neobank that benefited from a narrow geographic focus, operating only in Brazil for its first six years, where they have now gathered more than 95 million clients (making up 55% of the adult population) before expanding elsewhere. Other examples include KakaoBank with 24 million customers in Korea, and Monzo surpassing 10 million customers in the UK.

There are some notable exceptions like Wise and Revolut that pursued rapid international expansion. Revolut boasts a global footprint across 38 countries with 45 million customers as of June 2024.

Diversified revenue streams

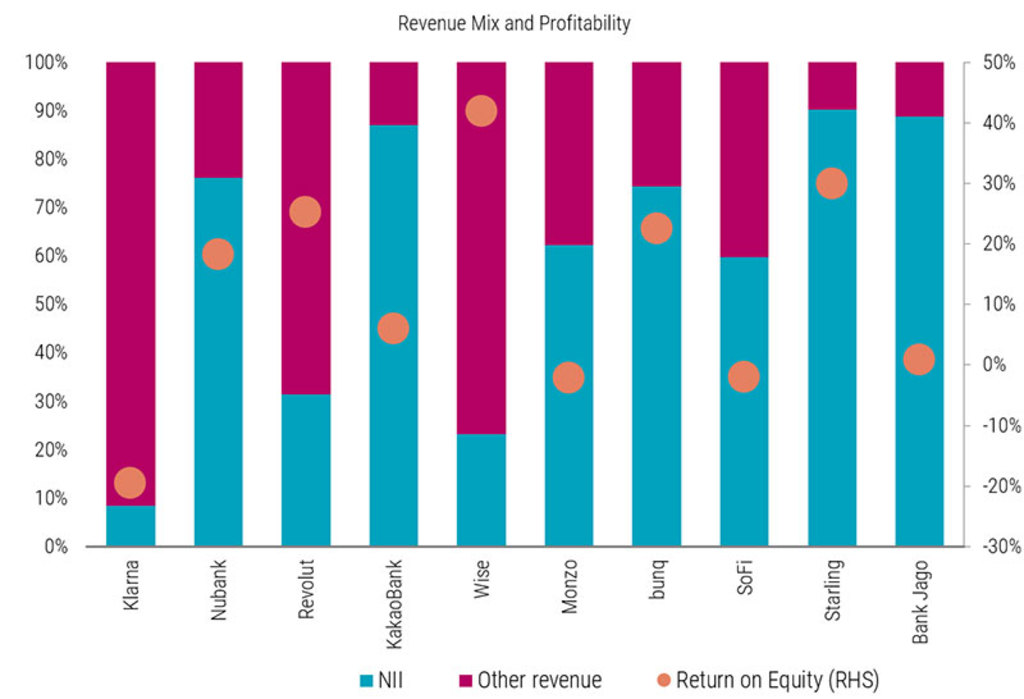

Establishing robust credit operations is a crucial factor. Nubank and Starling have established lending businesses and others are in the process of rolling out credit to their clients. Neobanks tend to focus more on unsecured credit, though there are some players offering mortgages (Starling in the UK, KakaoBank in Korea, Inter in Brazil). Revolut delivered strong profitability last year despite low reliance on credit (loan-to-deposit ratio at just 3.5%). This was due to higher interest on liquidity and strong revenue diversification, with no single product stream or region accounting for more than 30% of the top line.

Figure 3: Neobanks are very focused on diversified revenue streams, not just net interest income

Source: Robeco, company data, end December 2023

Continuous innovation

Lacking legacy tech and digital focus allow neobanks to rapidly launch and re-work new products and solutions. Revolut, which had only two products in 2015 (its flagship multi-currency travel card and a mobile app) now offers a full suite of services including investments, trading (including crypto) and credit. Revolut also has a dynamic approach to managing its products and cancels products/features based on customer feedback. Similarly Nubank expanded its offer from credit cards to personal loans, investments, cryptocurrency trading, auto and life insurance, among other product lines.

FinTech D EUR

- performance ytd (31-5)

- -14.54%

- Performance 3y (31-5)

- 5.99%

- morningstar (31-5)

- SFDR (31-5)

- Article 8

- Dividend Paying (31-5)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Focus on primary relationships

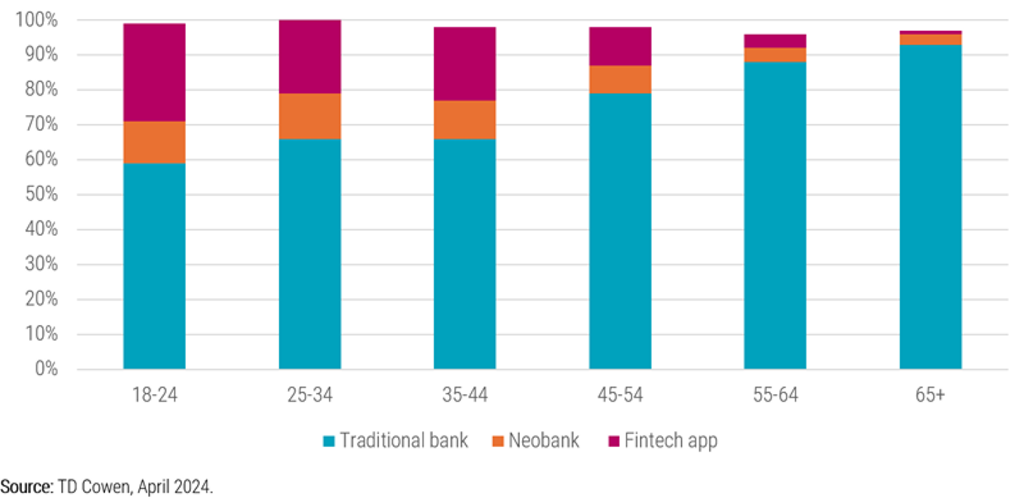

Neobanks attracted customers with the promise of a better user experience, but they are in the early stage of capturing primary banking relationships. According to data from EY, between 72% and 81% of consumers in the UK, France, and Germany say their primary financial relationship is with a traditional bank. Similarly, in the US consumers still predominantly use traditional banks for primary banking relationships, with 59% of the 18-24 age cohort and 93% of those over 65 (see Figure 4). Nubank stands out among peers, enjoying a primary banking relationship with 60% of its monthly active customers.

Figure 4: What type of company do US consumers use for their primary banking relationship?

Open your portfolio to the power of themes

For over 25 years, Robeco has been a pioneering leader in constructing thematic strategies.

Efficient customer acquisition

Successful neobanks tend to focus on customer-centric metrics like customer lifetime value and customer acquisition costs (CAC). Nubank managed to acquire approximately 80%-90% of customers through word-of-mouth or direct unpaid referrals, without the need for significant marketing expenses. As a result, CAC at Nubank remained broadly unchanged at <USD 1 in 2021-2023. Revolut saw 70% of new retail customers joining organically in 2023, however word-of-mouth growth was complemented by further investment into marketing and sales. As a result, the blended CAC doubled from ~GBP 10 per user in 2021 to ~GBP 20 in 2023, compared to GBP 9 for Wise (vs GBP 7 in 2021) with 66% of customer growth coming via word-of-mouth.

Conclusion

There is a large untapped market for neobanks with 1.5 billion unbanked and 2.8 billion underbanked adults across the world. While few neobanks are achieving profitability yet, successful business models with diversified revenue streams and a focus on innovation are well placed to deliver attractive returns. We invest in select neobanks in our Fintech strategy and are monitoring the private neobanks which could list in the future such as Chime, Klarna, and Revolut. We invested in Nubank at the time of the IPO after contact with management for more than a year. The investment has generated an annualized return of over 100%1 since Nubank turned profitable at the start of 2023, demonstrating the growing importance of this fintech segment.

Footnote

1 Robeco, 30 August 2024.