Impact Specialist

概要

- Influence and power of autocratic regimes may be weakening

- Democratic forces strengthen in Türkiye, but ESG performance still plummeting

- BRICS bloc still underperforming relative to potential

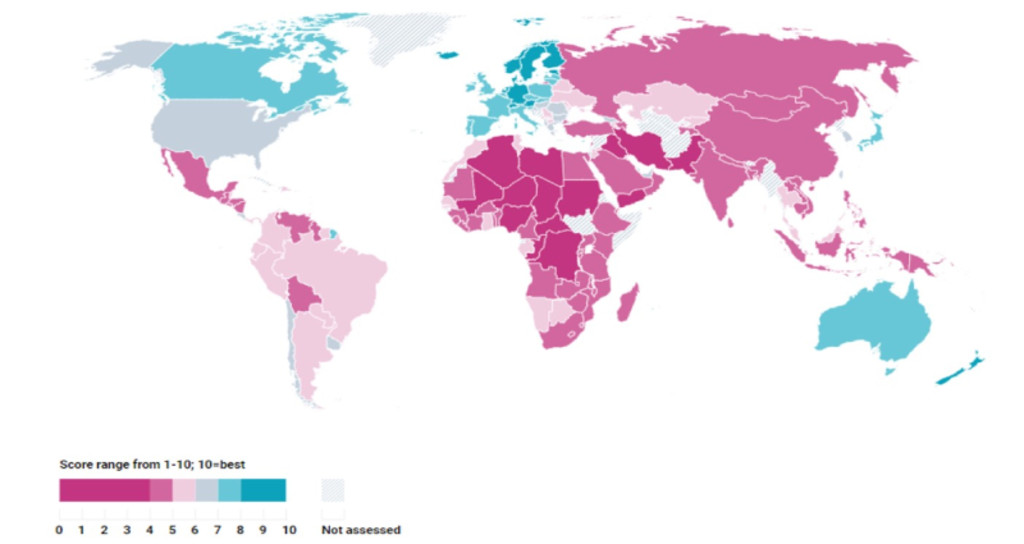

Finland narrowly edged out runner-up Sweden to retain the title of the world’s most sustainable country. Denmark overtook Norway for a spot in the top three while Switzerland, once again, rounded out the top five in the spring edition of the Country Sustainability Ranking.

With a five-notch move from October’s rankings, New Zealand broke into a top-ten traditionally dominated by European countries. Despite its emerging market status, Estonia ranked just below New Zealand at No. 11. The small Baltic state impressively maintains a sustainability performance that outshines bigger European economies including Ireland (No. 12), the UK (No. 13), France (No. 15), Luxembourg (No. 14) and Belgium (No. 24).

Moreover, climate and energy criteria continue to gain significance. Though some countries are making incremental gains, environmental scores continue to weigh down performance in multiple G20 countries including Canada (No. 16), Japan (No. 17) and Australia (No. 21). In contrast, better biodiversity and water efficiency marks helped elevate the US up slightly to position No. 36.

Sudan, Chad, and Libya in Africa and Iraq, Iran and Yemen in the Middle East rounded out the bottom of the 150-country list.

Figure 1: The global country sustainability ranking map¹

Data source: Robeco, country sustainability scores as of April 2023. Countries are color coded based on ESG scores.

Extreme inflation and a catastrophic earthquake helped galvanize a Turkish opposition, pushing it closer than ever to toppling the two-decade old regime of President Recep Tayyip. Though it mounted a formidable challenge, the opposition was, in the end, unable to release Türkiye from Erdoğan’s grip. The country’s deteriorating ESG position, which for decades has lagged emerging market peers, is set to continue its Erdoğan-era declines.

His authoritarian grip has left cultural, political, and economic institutions weak and unprepared for managing a dangerous mix of simmering environmental, social, and political risks. These include rising emissions, an aging population, reduced worker rights, constricted individual freedoms, and rampant corruption.

[Erdoğan’s] authoritarian grip has left cultural, political, and economic institutions weak and unprepared for managing a dangerous mix of simmering environmental, social, and political risks

Autocracy vs democracy

In addition to Türkiye, democracy has been under attack in regions across the world including Peru and Brazil in South America, Ethiopia and Tunisia in Africa, Myanmar and Thailand in Southeast Asia. However, these appear as mere skirmishes compared to Russia’s invasion of a sovereign Ukraine.

Meanwhile, China’s phenomenal rise in economic growth has challenged long-standing notions that democracy is superior to autocratic regimes. New research from the IMF counters those claims, showing that only a strong democracy provides the staples needed to spur innovation, advance economic development and build resilience to counter disruption. Moreover, recent results from Freedom House demonstrate that after two decades, the decline in democracy may have reached a nadir.

Japan’s aging demographics – an inverted pyramid

With nearly a third of its population over 65 and one of the world’s lowest fertility rates, Japan is staring at a demographic challenge of inverted proportions. Its old age dependency ratio stands at 51.2% (only the sunbaked, tax-light Principality of Monaco scored higher).

Aging demographics pose severe risks for public finances which Japan can scarcely afford. General government debt estimates for 2023 stand at 258% of GDP and are forecasted to reach 264% in 2028 – almost twice that of the US.2

Figure 2: An inverted pyramid – Japan’s aging demographics

The chart shows the age distribution of Japan in year 1950 and 2020 and a forward-looking projection for 2050 based on current demographic trends. The bulk of the population rising to the elderly age brackets forming an inverted pyramid.

Source: Robeco, UN Population Division

Australia – a renewed climate ambition

Catastrophic floods and droughts are punishing Australia with increasing regularity, pushing the government to intensify efforts to fight climate change. In 2022, Australia joined the Global Methane pledge for reducing emissions in waste and energy sectors, increased its Nationally Determined Contributions (NDC) originally pledged under the Paris Agreement, and signed emission reduction plans into national law. This year it’s banning the use of carbon offsets to pull down emission in high-polluting industries.

[In Australia], an accelerated and smooth transition requires the rapid reskilling and transfer of workers from the fossil fuel to clean energy sector

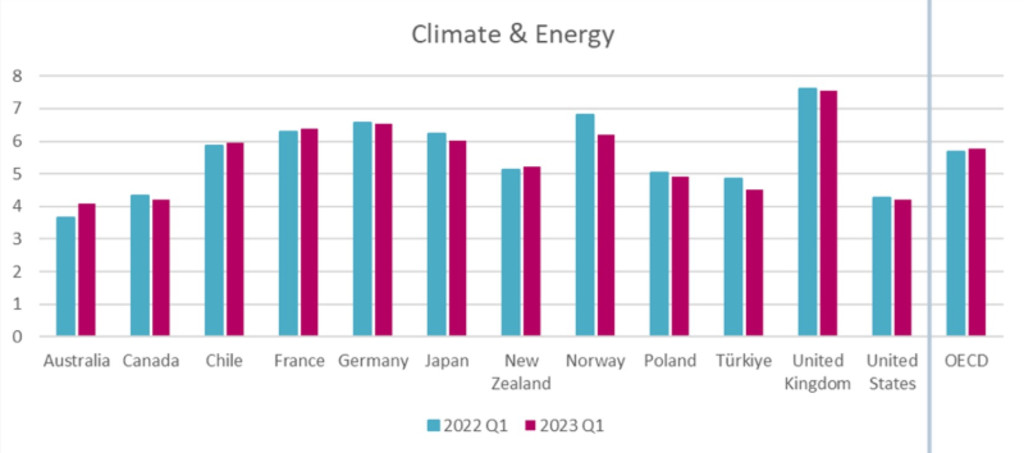

Though moving in the right direction, Australia still has a long way to travel given its status as one of the world’s highest carbon emitters3 (See Figure 3). Energy dominates its exports and generates nearly half (47%) of total domestic emissions. The shift to renewable production (from the current 27% to 82% in 2030) will carry high social costs. An accelerated and smooth transition requires the rapid reskilling and transfer of workers from fossil fuel jobs to the clean energy sector.

Figure 3: Australia worse-off than OECD peers for climate and energy

The chart displays Australia’s performance on the ‘Climate and energy’ criterion compared with that of major OECD countries and the OECD average comprised of 37 countries.

Data source: Robeco; data assessed as of April 2023

South Africa – untapped potential

Thanks to small gains in biodiversity, aging and political stability, China, India and Brazil saw small increases in scores and ranks. Still, the BRIC-bloc all scored in the lower half of the sustainability rankings, falling well short of their ESG potential. South Africa in particular is struggling.

Over the last year, South Africa has faced a series of crises. Infrastructure deficiencies have led to crippling power outages, extreme weather to water supply shortages, factional infighting to the worst civil unrest since the collapse of apartheid. Meanwhile, the Covid pandemic and continued geopolitical tensions abroad have hampered food imports, exacerbated already rampant income inequalities and slowed economic growth and development.

The one-time poster child for the economic power of emerging markets has over decades failed to address serious obstacles to growth including high unemployment, rampant corruption and insufficient investments into physical and social infrastructure. Even after more than five years in office, its current president Cyril Ramaphosa has been unable to enact meaningful reforms and sustainability performance as well as its sovereign credit rating have seen a steady state of declines since early-20094.

Footnotes

1 Complete scores and rankings can be obtained for free via Robeco’s SI Open Access portal. Visit Robeco’s global website for more information.

2 IMF Debt Map, https://www.imf.org/external/datamapper/GGXWDG_NGDP@WEO/JPN/CHN/DEU/USA

3 Based on OECD averages.

4 In 2007 and much of 2008, South Africa enjoyed investment grade credit ratings. Currently, the country is classified as sub-investment grade by Fitch (BB-), S&P (BB-), and Moody’s (Ba2).

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.