Impact Specialist

• 市場觀點

Finland slips, while environmental risks ripple in the latest country sustainability rankings

In Robeco’s latest Country Sustainability Report, Finland slipped slightly to tie with Sweden for the country with the best ESG scores. Meanwhile, rising emissions and intensifying weather events are reducing resilience and raising the stakes of environmental risks for developed and developing countries alike.

概要

- Nordic nations + Switzerland still own the top ESG slots

- Physical risks of climate change are gaining traction

- Greece’s ESG scores and economic growth rise from the ruins

The report, released in the spring and autumn each year, tracks the sustainability risk and performance of 150 countries on more than 50 indicators covering environmental, social and governance factors. The results give investors – especially of sovereign bonds – and stakeholders a comprehensive look of the emerging risks and opportunities that are frequently overlooked or underappreciated by markets.

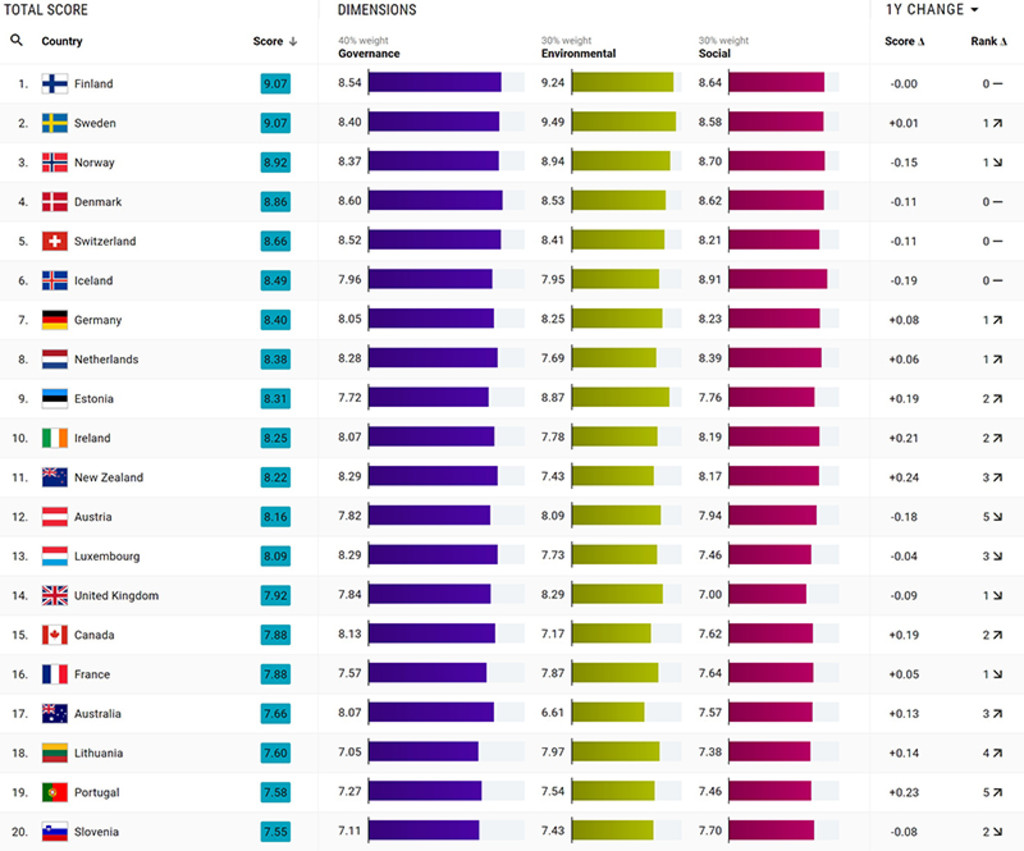

In this edition, Scandinavia once again shined. Sweden tied with Finland for first (both scoring 9.07), followed by Norway and Denmark. Switzerland squeezed ahead of Iceland to round out the top five positions. The tie at the top stemmed from a slight Finnish falter on climate and energy as well as on water and waste management criteria – critical components of the environmental score. Improved environmental performance was also crucial in moving Estonia and Ireland into the group of top ten, bumping out Austria and New Zealand. Both countries suffered downgrades on socioeconomic variables, including aging for Austria and income inequality in New Zealand.

Figure 1 | Top 20 Country Sustainability Ranking

Source: Robeco, October 2023

Meanwhile, war continued to depress the ESG scores of not only Russia but also Ukraine. Russia dropped 18 spots to rank at 123; Ukraine fell by 24 spots to position 87. Behind these, rankings for Djibouti, Nicaragua and Kazakhstan also saw significant double-digit drops.

The biggest movers in the last six months came from the lower end of the ranks, with many coming out of Africa. Mongolia, Niger, Laos, Uganda and Angola (whose places range from 86 to 117), all saw significant gains in their overall ranks, thanks in large part to improving environmental scores. The middle of the ranks also had some momentous movers including Taiwan, the United Arab Emirates (UAE), Botswana, and Jordan which now enjoy new positions ranging from 37 to 58, respectively.

The largest losses over the past six months came from Malta, Kuwait and Libya (the lowest ESG performer), all of which suffer from chronically deteriorating environmental performance.

Climate risks are building strength

Being an economic heavyweight doesn’t protect against poor environmental performance. ESG scores of both Japan and the US took a tumble on the back of weak regulatory policies and growing industrial emissions. Weaker ‘E’ scores also reflect a larger exposure to natural catastrophes that cost lives, while also lowering productivity and disrupting economic output.

Emissions-induced climate change will continue to scramble weather patterns, increasing the frequency and magnitude of natural catastrophes globally. The US battled wildfires on its western coast and hurricanes in the East. As an island nation, Japan and its densely populated cities, are particularly exposed to tsunamis and dangerous seawater surges from ocean storms. In 2022, the global economic damage from natural disasters was estimated at USD 220 billion, with extreme weather responsible for roughly half the total.1

Rising emissions and intensifying weather events are reducing resilience and raising the stakes of environmental risks

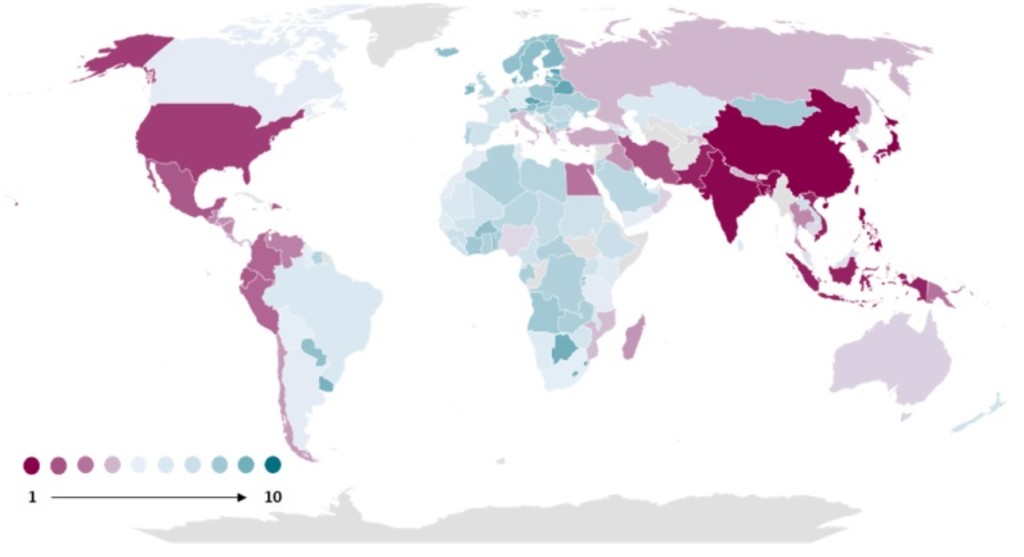

For developing nations with smaller and less resilient economies, catastrophic events are disproportionately devastating to economic development. Underscoring the importance of these events for sustainable development, the United Nations devoted SDG indicator 11.5.2 to measure the economic losses from natural disasters relative to GDP.

While they cause serious damage, storm flooding is a short-term problem. Rising sea levels from melting polar icecaps present longer-term risk which will carry significantly larger costs for any country with a coastline.

Figure 2 | Countries with the greatest risk for natural disasters

1 = areas with higher risks of natural hazards and disasters, 10 = areas facing lower catastrophic risks

Source: Robeco, October 2023

The BRICS bloc is building out

With the proposed addition of Argentina, Ethiopia, Egypt, Iran, UAE, and Saudi Arabia, the BRICS bloc is on a path to get a lot bigger. Though the long-term implications are still unclear, the bloc’s worldwide economic and geopolitical influence should expand. Its citizens currently number 3.7 billion – nearly half the global population (46%), and its combined GDP stands at nearly USD 26 trillion – more than a quarter of global economic output. Equally important is its share of global oil production which will swell from 20.4% to 43.1%.

With the exception of Ethiopia, which is slowly recovering from a brutal civil war, all proposed new joiners saw rises in ESG scores. Argentina’s stronger score is of particular interest, given the social, economic and political turmoil it has faced in recent years. As South America’s second-largest country by land mass and third largest by population, Argentina is a major emerging market with significant risks but also significant potential.

Argentina – Milei’s impact on the momentum

In its favor, Argentina boasts high volumes of natural lithium reserves, a critical element that will enable the electrification and energy transition of the global economy. That said, its own economy is highly dependent on agriculture, leaving it overly exposed to weather vagaries and unpredictable commodity prices. Recent droughts that reduced harvest forecasts further underscore this threat.2

Despite these risks, Argentina has improved on all three ESG dimensions and its overall score; whether those gains will continue is hotly contested. In late November it elected right-wing libertarian Javier Milei as president, creating uncertainty for its ESG profile. Social scores are particularly vulnerable, given Milei intends to slash subsidies and drastically reduce social expenditures. 3

Ode to a Grecian ‘turn’

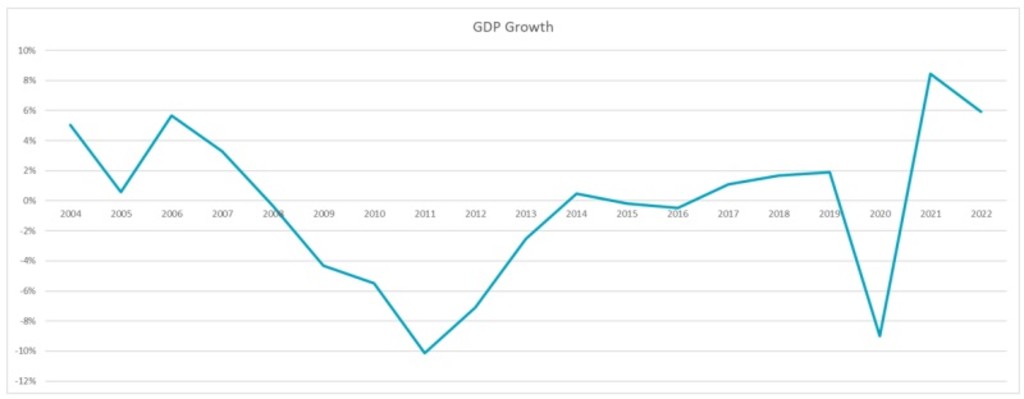

Whatever the fallout, Argentina can take comfort in Greece’s heroic rebound from the brink of default more than a decade ago. The downgrade of its sovereign bonds in early 2011 was presaged by declines in its overall ESG scores already in 2008. Since then, Greece’s E, S, and G scores have steadily improved from a nadir in 2014 – improvements that have coincided with social reforms, fiscal prudence and economic growth. In 2021 and 2022, Greece’s economy grew at twice the Eurozone average, and unemployment, while still high at 11%, is currently the lowest in over a decade.

Figure 3 | Out of the ruins – Greece’s annual GDP growth (%)

Source: The World Bank4 , 2022

For more details on country scores and rankings, visit Robeco’s SI Open Access Portal.

Footnotes

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.