PhD, Head of Sustainable Index Solutions

• Visión

Indices insights: To what extent can carbon emissions data identify climate leaders and laggards?

Carbon emissions do not tell the full story on companies’ climate change awareness. That said, investors routinely rely on carbon metrics to track progress on their decarbonization objectives. In this Indices insights article, we analyze to what degree climate leaders and laggards can be identified using carbon footprint measures.

Autores/Autoras

PhD, Portfolio Manager Sustainable Index Solutions

Climate & Biodiversity Strategist

Climate Data Scientist

Top keywords

Resumen

- Carbon footprint measure quantifies past or current greenhouse gas emissions

- The metric is less useful for identifying climate leaders and laggards

- Additional climate data that captures other dimensions is needed to discern between the two

As climate change becomes a key issue for most investors, the focus on carbon footprint reduction in investment portfolios has increased and net-zero commitments have moved into the mainstream.1 In response, industry players have developed several low-carbon investment vehicles and Paris-aligned benchmarks. What these have in common is the exclusion of companies with high carbon emissions or intensities.

Undeniably, generic carbon emissions data is useful for mapping out portfolio-level or entity-level decarbonization pathways. However, this begs the question of whether the simple approach of excluding or divesting from high carbon emitters is the most effective mechanism to transition to a low-carbon economy. In other words, it is worth examining whether the information gleaned from carbon emissions data suffices for identifying climate leaders and laggards.

Recent research shows that green innovation is primarily driven by the energy and materials sectors, two of the most carbon intensive industries.2 Within these segments, however, the more innovative firms do not necessarily have the lowest carbon emissions or intensities. As such, carbon emissions data alone is unlikely to be an effective guide to identifying firms involved with green innovation, or to distinguish between climate leaders and laggards, as it only considers past or current emissions.

An alternative approach to pinpointing climate leaders and laggards is to assess how firms impact specific climate-related SDGs. For example, Robeco’s proprietary SDG framework can be used to evaluate the contributions companies make to these SDGs, taking into account what they produce and how they operate. The resulting SDG scores then indicate if the firms positively or negatively impact the relevant climate-related SDGs, and to what extent.

Carbon emissions data is not useful in distinguishing between climate leaders and laggards

To evaluate this notion, we analyzed the relationship between climate leaders/laggards and their respective carbon footprints. Specifically, we looked at the intersection of companies that have low carbon footprints and either low or high climate-related SDG scores, and the intersection of firms that have high carbon footprints and either low or high climate-related SDG scores.

If carbon emissions data is a sufficient measure to differentiate between climate leaders and laggards, we would expect low carbon footprint companies to highly overlap with high climate-related SDG scores, and high carbon footprint companies to highly overlap with low climate-related SDG scores.

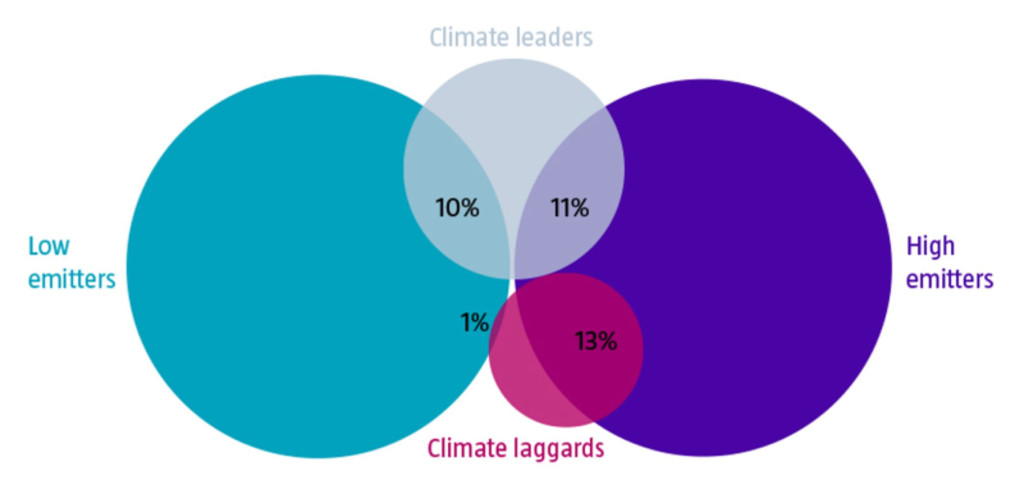

Figure 1 | A significant number of climate leaders/laggards are not identified with the use of carbon footprint data

Source: Robeco, TruCost. The analysis is conducted using data as of end of December 2021.

As shown in Figure 1, we found that carbon emissions data is too crude to effectively differentiate between climate leaders and laggards on an issuer level. While 13% of high emitters are considered climate laggards, there is also a considerable share of 11% of high emitters which are viewed as climate leaders. Put differently, a low-carbon approach that relies solely on carbon footprint data for exclusions or divestments is also likely to ignore high carbon-emitting firms which, in fact, contribute positively to the climate-related SDGs and are deemed essential for the transition to a low-carbon economy.

Focusing on the group of low emitters based on carbon emissions, a portion of 1% are seen as climate laggards as these companies contribute negatively to the climate-related SDGs. But more strikingly, only 10% of low emitters are classified as climate leaders, less than the share of climate leaders within the high emitters cluster. This suggests that carbon emissions data is ineffective in identifying firms involved with green innovation. Therefore, complementary stock-level climate data is required to achieve this goal.

Subscribe - Indices Insights

Receive an update as soon as a new article is available with insights about sustainability, factors or markets.

Data and methodology

For our analysis, we based our investment universe on the constituents of the MSCI World Investable Market Index (MSCI World IMI) as at the end of December 2021. We used carbon footprint data sourced from TruCost, defined as Scope 1 and 2 divided by enterprise value including cash (EVIC).

We used SDG scores based on Robeco’s proprietary SDG framework. We focused only on certain climate-related SDGs, specifically SDG 7 (affordable and clean Energy), SDG 11 (sustainable cities and communities) and SDG 13 (climate action). To calculate the final climate-related SDG score, we took the lowest of the three scores if one of them was negative, and the highest of the three scores if they were all positive. Combined, this analysis covered 73% of the stocks and 85% of the total market capitalization of the MSCI World IMI.

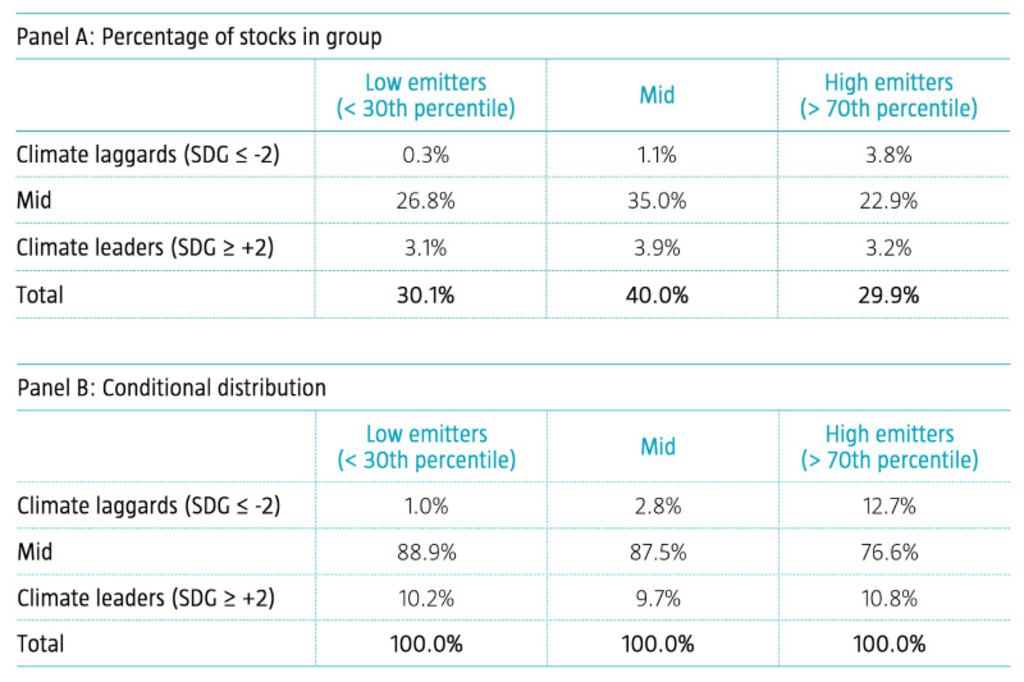

We then sorted stocks into 3x3 mutually exclusive groups based on their carbon footprints and climate-related SDG scores. For carbon footprints, we grouped stocks using the 30th and 70th percentiles. Companies that had a climate-related SDG score of -3 or -2 were classified as climate laggards, and those with a climate-related SDG score of +2 or +3 were classified as climate leaders. Panel A in Table 1 depicts the percentage of stocks that belonged to each of the nine groups. Panel B shows the conditional distribution on the carbon footprints.

Table 1 | Distribution of stocks sorted on carbon footprints and climate-related SDG scores

Source: Robeco, TruCost. The analysis is conducted using data as of end of December 2021.

Based on the conditional distribution, we constructed proportional Venn diagrams. These display the overlap between high emitters and climate laggards, high emitters and climate leaders, low emitters and climate laggards as well as low emitters and climate leaders. The total area of the circles are proportional to the number of stocks that belong to a group.

Conclusion

While carbon footprint is a useful metric for mapping out portfolio-level or entity-level decarbonization pathways, we find that it is less effective in differentiating between climate leaders and laggards. Indeed, a significant number of climate leaders and climate laggards are not identified using this measure. For this purpose, we suggest complementing carbon footprint measures with additional stock-level climate data that captures dimensions in addition to emissions.

Footnotes

1 See: Robeco, March, 2022, “2022 global climate survey”, Robeco publication.

2 See: Cohen, L., Gurun, U.G., and Nguyen, Q., January 2021, “The ESG-innovation disconnect: evidence from green patenting”, SSRN working paper, and Huij, J., Laurs, D., Stork, P. A., and Zwinkels, R. C. J., November 2021, “Carbon Beta: A market-based measure of climate risk”, SSRN working paper.

Background to sustainability metrics

In defining sustainability, investors have a multitude of dimensions and metrics they could consider. For example:

Values-based exclusions

ESG integration

Impact investing

ESG scores typically put more focus on the operations of a business, whereas SDG scores also incorporate the impact that the business’ products and/or services have on society.

We see client sustainability objectives increasingly moving towards avoiding controversial businesses (values-based exclusions) and including those that provide sustainable solutions (impact investing). In the first few articles of our Indices Insights series, we will empirically show how the different sustainability metrics (negative screening/exclusions, ESG, SDG) relate to these increasingly impact-oriented client sustainability objectives.

The Indices insights series provides new insights focused on index investing, particularly on the topics of sustainable investing, factor investing and/or thematic investing. The articles are written by the Sustainable Index Solutions team and often in close cooperation with a Robeco specialist in the field. The team has vast experience in research and portfolio management and has been designing sustainable, factor and thematic indices since 2015 for a large variety of clients: sovereign wealth funds, pension funds, insurers, global investment consultants, asset managers and private banks. The team can also tailor sustainable indices to cater to client-specific needs. For more information please visit our website Sustainable Index Solutions (robeco.com).